How Chip works, according to Chip

Interest rates on savings are so rubbish right now, that I’m keen to find different ways of making the most of our money.

As the rates on savings accounts and high interest current accounts limbo even lower, turns out there’s a solution on your smartphone.

I opened a fistful of current accounts to earn extra interest, only for the banks to turn round and slash the rates. Cheers for that Santander, Lloyds and TSB.

Now it looks like the Chip savings app can help me earn more interest, on more money, than I could with the current accounts.

Whoop whoop! (I’m easily pleased).

So after I signed up for Chip back on March 2, here’s what I reckon so far:

Table of Contents

What is Chip?

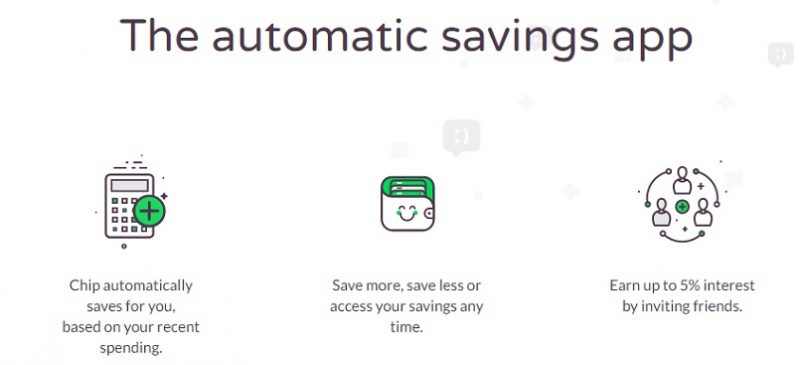

Officially, Chip touts itself as an “automatic savings app”.

You let Chip take a dekko at your current account, and it uses whizzy algorithms to analyse your spending patterns, and tot up how much you can afford to save. It then transfers small amounts of money every few days into a Barclays savings account.

This is all well and good, and could definitely help people save more than if they waited until the end of the month, looked at what little was left, and didn’t get round to saving it.

It also takes away the fear that if you set up a standing order to a savings account each month, you risk not having enough left to pay your bills. Plus, it sounds great if your income and expenses vary a lot each month (hands up all freelancers).

However, the bit that really interested me is that you can earn up to 5% a year interest.

YES PEOPLE 5%.

Persuade other people to sign up with your own referral code, and your rate gets bumped up by an extra percentage point per person, to a maximum of 5% a year.

They used to offer the option of £10 each in cold hard cash when signing up with a referral code, but now it’s just 1% interest each.

Plus – you can earn the interest on up to £10,000!

You don’t have to wait for the app to make savings, but can tell it to shovel across up to £100 a day, up to six times a month, yourself. Do that for long enough, and you could end up with a tidy sum earning 5%. Sure, if it gets too popular, Chip might change the rules. But right now, that sounds pretty good to me.

Interested? Read on for what I think is good and not so good about Chip.

WHAT’S GOOD

The chance of 5% interest

Seriously folks, this is pretty much as good as it gets on cash savings. Nearest you’ll get otherwise is 5% on a Nationwide FlexDirect current account on a maximum of £2,500, and that only lasts for a year. With Chip, keep on shovelling across £100 six times a month, and you can rack up the interest on up to £10,000.

The app is quick and easy to download and set up.

You can find it here for iPhones and here for Android. Then claim 1% interest by using the code 4T0C9I.

Saving is incredibly quick and easy

Seriously, you can save £100 with just 12 touches on your smartphone screen, and that includes typing in a 5 digit passcode. I’ve saved first thing in the morning, while jogging and at a jazz club (don’t judge). Otherwise, if you don’t want to transfer lump sums, you can just leave Chip to do its thing without doing anything further.

The online support is quick and easy to access

It’s just like typing a text or Facebook Messenger exchange. You don’t have to wade through pages of “contact me” forms, and “have you checked out our FAQS?” and “we aim to answer your email in 24 to 48 hours” like normal internet banking. Admittedly, Chip probably doesn’t have gazillions of customers right now, but the live customer support is working pretty well at the moment.

Your money goes into a Barclays savings account in your name

Rest easy, because your hard earned cash doesn’t end up in some strange bank account in the Caymans. If Chip goes bust, you can still get your money from Barclays. If Barclays goes bust, you have bigger problems on your hands because saving this way isn’t covered by the Financial Services Compensation Scheme. So let’s keep our fingers crossed that we don’t face a financial apocalypse that sees Barclays going to the wall, eh.

It promises not to take too much

Chip is so confident that the whizzy algorithms won’t get it wrong, that if it makes an automatic saving that pushes you into your overdraft, it promises to replace the money immediately, pay the bank charges, and pop £10 in your savings account to apologise. You also get notified of transfers, and can cancel, pause, increase or decrease them if you want to.

You can get your money back pretty quickly

According to the Chip website, if you ask to withdraw money before 2pm, you’ll have it back in your current account that afternoon. After 2pm or at the weekend, and you’ll have to wait until the next working day. I haven’t tried withdrawing anything yet so can’t confirm this.

WHAT’S NOT

It’s only a chance of 5% interest

You’ll only earn that much if you can persuade other people to sign up with your referral code. Plus, the extra interest only works for a year. Come year two, it drops back to 0% and you’ll need to persuade more people to sign up if you want to keep earning higher rates.

Although you can only earn a maximum of 5%, I was told by Tali on Chip live chat that if you get more referrals during the year, you can keep asking for an extra 1% interest and it will be “queued up” ready for the next year. All depends which is worth more to you – the prospect of extra interest or cold hard cash in your hand!

You can’t automate the £100 a day process.

Nope, you’ll have to resign yourself to transferring £100 a day, and remember to do it six times a month, until you run out of spare hundreds. Rats. Plus, it resets every 24 hours, rather than at a set time of day or night. Think about that – it means if you tell it to save at 7am one day, you have to wait till after 7am the next day. Forget to do it till later, and you’ll have to wait until later every day after that too.

There’s a big time delay between you telling the app to save, and the money actually hitting your savings account.

If you’re used to normal internet banking, where the money can switch between accounts faster than you can open browser windows, then Chip is positively glacial. Part of that is because the transfer takes place by direct debit, and Chip says it has to give you a day to cancel a save, and then wait 48 hours before instructing the Direct Debit transfer. In practice it takes even longer than that – currently I have 6 days’ worth of transfers pending.

If you make savings yourself, it delays the automatic savings

If you tell Chip to transfer a lump sum, as I’ve been doing with my £100 transfers, the algorithms throw a wobbly and won’t do any automatic saving for a week or so.

Prepare for emoji overloand

Chip is targetted fair and square at millenials who’ve never known life without the internet and a smartphone glued to their hand. If you’re going to use it, brace yourself for extra emojis, bad puns and gifs aplenty. The most disturbing one is a flirtatious Paul Hollywood.

It only works with 12 banks currently

Fine if you’re with one of the big banks, not so good if you use for example Tesco Bank.

The accounts that are included are (big breath): Barclays, Co-operative Bank, First Direct, Halifax, HSBC, Lloyds, Metro Bank, Nationwide, NatWest, RBS, Santander and TSB.

You can only link to a single bank account

If your banking is a tangled mix of standing orders and direct debits from multiple accounts, it won’t cover them all, but only one of them. So choose carefully.

The interest is only paid every three months

If you take money out of your savings account just beforehand, you won’t get credited with any unpaid interest on the withdrawal. So sure, you can get hold of your money quickly, but you’ll need to think about the timing if you want to make the most of your interest payments.

You’re giving an app access to your bank account data

Chip bangs on about encryption and security and data control licences, but fundamentally if you’re paranoid about internet banking this won’t work for you. Also, you’re letting a company look at all your transactions. It may be read only, but they can see what you pay to whom, with the risk of unleashing mammoth amounts of targetted junk mail in future. If you avoid supermarket loyalty schemes because you don’t want someone analysing your spending patterns, steer clear of this too.

Don’t do it if you’re in debt

As with any savings, it’s a bad idea to build up savings if you owe expensive debts elsewhere. If you’re paying more interest on debt than you earn on savings, I suggest using any extra cash to pay down debt first.

Who knows how long it will last?

Just as the banks chopped the rates on high interest current accounts, so Chip could decide at any point that it’s lured in enough customers, and cut the interest paid. Get in fast and grab any interest while you can, I say.

So – over to you? Any interest in saving by smartphone?

And if you do want to try Chip, whether for iPhone or Android, do consider using my 4T0C9I referral code, so you earn 1% interest (and I will too).

Great app, saved over £700 since OCT 16. Money is held in Barclays ACCT so completely safe.

I lost my job and there was no way to get income for my family, things was so tough and I couldn’t get anything for my children, not until a met a recommendation on a page writing how Mr Bernie Doran helped a lady in getting a huge amount of profit every 6 working days on trading with his management on the cryptocurrency Market, to be honest I was skeptical at first but I took the risk to take a loan of $500, and I contacted him unbelievable and I was so happy I received a profit of $5,500 with an investment of $500 within 7 days of trading , the most joy is that I can now take care of my family, i am just sharing my testimony on here. I don’t know how to appreciate your good work Mr. Bernie Doran, God will continue to bless you for being a life saver I have no way to appreciate you than to tell people about your good services. He can also help you recover your lost funds, For a perfect investment and good return on investment contact him on Gmail : Berniedoransignals@gmail.com or his whatsApp + 1 ( 424 ) 285 – 0682

tell him i referred you

Very effective way of saving money very good saving rates which can go upto 5%. Use a referral code and get extra 1% interest plus FREE £10. I can defo see myself saving some extra money every month

Hi All

I am now using Chip for a few weeks now after reading this and love it

Its easy to set up and easy to use

Sam

I’ve been teetering on the edge with this type of savings app for a while and I’m now in a position to save some cash so I will give this a try. Great summary of info, thanks

Ok, I’m going to try this as I have maxed out my Help to Buy ISA allowance and Nationwide 5% – sounds good to me! I’ll let you know how I get on. L x

I keep looking at Chip. It looks and anything app wise I can use works for me! 5% interest is also fab as like you said, saving rates are dire right now. I might have to look into Chip more! Thanks for he heads up!!

I’ve never heard of Chip before, sound like it’s worth a try x

I’ve not heard of this before but it does certainly sound interesting

I love the idea of this, it sounds so simple too which suits me! Might sign up, thanks for sharing

Hi All,

Chip is fantastic, have been using it a while now, what a great way to save!

When you sign up, it will ask for a referral code. If you enter the below code:

…you can get an increase of 1% HIGHER interest rate 😉

Hope this helps!

Tyler – delighted that you’ve had a great experience with Chip and thanks for commenting.

However, will point out that Much More With Less readers using MUCH3 can start earning higher interest at 3%, rather than the 1% with your referral code, so I will remove it.

Chip is pretty good, I’ve managed to save quite a bit without really realising and I was a completely miserable saver before.

Big fan of Chip, cheers!

Hi,

Please use this code to give yourself an extra 1% interest when signing up to the awesomeness that is Chip:

H2P53W

Cheers,

Tom

Love the app! I have been using it for 1 year and have saved about £1k, which I am going to use for my next holiday. 😉 Also found about Emma, the budgeting app, which I use in parallel. Looking forward to saving my next £5k. ehhe

Your post highlights the potential of becoming a freelance proofreader or editor for authors, publishers, or businesses looking to ensure the accuracy and professionalism of their written content. For more information, click here.

Want to make money by offering virtual marketing consulting? click here and uncover strategies to help businesses improve their marketing strategies.

Looking for a way to make money through online surveys? click here and uncover platforms that offer paid surveys and rewards for your opinions.

Thank you for addressing the potential of creating and selling stock photos or graphics as a way to generate income. It’s a creative opportunity for photographers and designers. click here for more information.

I appreciate the emphasis on the importance of managing time effectively when pursuing money-making opportunities. It’s a resource we all have and can leverage wisely. For more information, click here.

I appreciate the effort you put into explaining this topic. To explore further, click here.

Your post highlights the potential of creating and selling stock photos or illustrations through online platforms like Shutterstock or Adobe Stock. It’s a way to monetize your creativity and generate passive income. For more insights, click here.

Earn $50 by completing the above task

Your post emphasizes the importance of providing value and solving problems for your customers or clients when pursuing money-making opportunities. It’s a customer-centric approach that leads to success. For more information, click here.

Thank you for highlighting the importance of financial literacy and educating oneself about money management. It’s an essential foundation for long-term financial success. click here for more details.

Your post emphasizes the importance of earn money online.For more details,Click here.

Your post emphasizes the importance of online earning.For more details,Click here.

Your post emphasizes the importance of .For more details,Click here.

Your post emphasizes the importance of make money online.For more details,Click here.

Your writing style is clear and concise, making complex and useful concepts accessible to readers. It’s easy to follow and understand the strategies you’ve shared. To delve deeper, click here.

Your post emphasizes the importance of make money online.For more details,Click here.

Your post emphasizes the importance of make money online.For more details,Click here.

Your post was very good emphasizing the importance of making real money online. For more details,Click here.

Your post emphasizes the importance of make money .For more details,Click here.

Your post emphasizes the importance of make money online.For more details,Click here.

Your post emphasizes the importance of earn mony online.For more details,Click here.

Your post emphasizes the importance of Earn money from the comfort of your own home.For more details,Click here.

Your post emphasizes the importance of make your online mony.For more details,Click here.

Your post emphasizes the importance of make money online.For more details,Click here.

Your post emphasizes the importance of make money online.For more details,Click here.

I just want to say Thank You to everyone who supported me through the years. My name is Manuel Franco, New Berlin, Wisconsin. My story of how I won the Powerball lottery of $768.4M is a bit of a tale. I have been playing Powerball tickets for 6 years now since I turned 18. I bought my first ticket on my 18 birthday. I was feeling very lucky that day because I had contacted Dr. Odunga Michael to help me with the winning Powerball numbers. I really had that great great feeling that I looked at the camera wanting to wink at it. I only did a tiny part of it and trusted him. He gave me the numbers after I played a couple other tickets along with it for $10. I checked my ticket after the winnings came online and saw the numbers were correct including the Power play. I screamed for about 10 minutes because it felt like a dream. I had won $768.4M. You can check my winning testimony with the lottery officials just with my name search. Thank you Dr Odunga. Well, his email is odungaspelltemple@gmail.com and you can also call or Whats-app him at +2348167159012 so you guys can contact him

Your post emphasizes the importance of Earning online money.For more details,Click here.

Your post emphasizes the importance of make money online.For more details,Click here.

Your post emphasizes the importance of make money online.For more details,Click here.

Your post emphasizes the importance of Earn money online.For more details,Click here.

Your post emphasizes the importance of make money online.For more details,Click here.

Want to make money through online tutoring? click here and discover platforms that connect you with students seeking academic assistance.

Your post emphasizes the importance of Make money online .For more details,Click here.

Your post emphasizes the importance of Earn money online.For more details,Click here.

Are you a skilled UI/UX designer? click here and explore opportunities to offer your design services for websites, mobile apps, or software interfaces.

Your post highlights the potential of leveraging social media influencers or affiliate marketing to promote products and earn commissions. It’s a collaborative approach to making money. For additional details, click here.

Real spell casters are hard to find but I am happy to thank Lord Krish for helping me win the lottery successfully after trying so many spell casters and I found my happiness in Lord Krish. I was given the lottery numbers by him which made me the third highest lottery winner in history and this is all thanks to you sir. Winning the lottery is something everyone would like to feel especially with a trustworthy spell caster. I, Yanira Alvarez, won the Powerball lottery in Los Angeles and I really thank Lord Krish because after I contacted him, he told me to only provide the spiritual items for him to do it for me and I didn’t hesitate to give him what he required so I could win it. I have tried so many spell casters who seemed real but only Lord Krish numbers gave me the winnings. I won the Powerball Jackpot of $1.08 billion and I am here today to share my experience to those willing to win the lottery as well. Take this opportunity to contact Lord Krish Spiritual with his email: lordkrishshrine@gmail.com and also share your experience with others.

VISIT GEO COORDINATES RECOVERY HACKER TO GET YOUR MONEY, STOLEN FUNDS, OR BTC RETURNED?

My purpose out here today is to share this article to the world about how GEO COORDINATES RECOVERY HACKER helped me in getting my lost funds back. Losing your life savings to scammers it’s not a good feeling, I lost everything, even sold some properties, I didn’t even know where to start from, I invested $72,000, which i was promised to get my first 15% profit in weeks, when it’s time to get my profits, I got to know the company was bogus, they kept asking me to invest more and i ran out of patience then requested to have my money back, they refused to answer nor refund my funds. I had contacted a few crypto recovery agents but they were all unprofessional not, until a friend of mine introduced me to this hacker called GEO COORDINATES RECOVERY HACKER. It gladdens my heart to be out here to share with you my incredible experience working with the recovery hacker called GEO COORDINATES RECOVERY HACKER. I must confess that it was the best decision that I made because my stolen Bitcoin was successfully returned to me. So for those who are victims, don’t let those unfortunate scammers get away with your hard-earned money. You can rely on your expertise. They have previously handled many successful cases. In order to get your stolen assets recovered Kindly contact them via

Email: (geovcoordinateshacker@protonme)

Email: (geovcoordinateshacker@gmail.com)

WhatsApp ( +1 (512) 550 1646)

Website; https://geovcoordinateshac.wixsite.com/geo-coordinates-hack

I don’t even understand how I ended up here, however I assumed this post was once good. I do not recognize who you’re but definitely you’re going to a well-known blogger if you are not already 😉 Cheers!

Yeah bookmaking this wasn’t a high risk conclusion great post! .

You made some first rate points there. I looked on the web for the difficulty and found most individuals will go along with together with your website.

I have been browsing on-line more than three hours as of late, but I by no means discovered any interesting article like yours. It is lovely price sufficient for me. In my opinion, if all website owners and bloggers made just right content as you probably did, the net will likely be a lot more useful than ever before.

Very efficiently written article. It will be supportive to everyone who usess it, as well as me. Keep doing what you are doing – for sure i will check out more posts.

I was recommended this website by way of my cousin. I’m not positive whether this post is written by him as nobody else understand such distinctive approximately my trouble. You are incredible! Thanks!

Hi there! I could have sworn I’ve been to this blog before but after browsing through some of the post I realized it’s new to me. Anyways, I’m definitely happy I found it and I’ll be bookmarking and checking back often!

Absolutely indited articles, Really enjoyed looking at.

I’ve been absent for a while, but now I remember why I used to love this site. Thanks, I?¦ll try and check back more frequently. How frequently you update your site?

I went over this website and I conceive you have a lot of superb info , saved to fav (:.

After all, what a great site and informative posts, I will upload inbound link – bookmark this web site? Regards, Reader.

Thank you for sharing excellent informations. Your site is so cool. I’m impressed by the details that you have on this website. It reveals how nicely you perceive this subject. Bookmarked this website page, will come back for extra articles. You, my pal, ROCK! I found just the information I already searched all over the place and simply could not come across. What a great site.

I love your blog.. very nice colors & theme. Did you create this website yourself? Plz reply back as I’m looking to create my own blog and would like to know wheere u got this from. thanks

You actually make it seem really easy together with your presentation however I in finding this matter to be really one thing which I believe I’d by no means understand. It kind of feels too complicated and extremely extensive for me. I’m having a look forward on your subsequent publish, I¦ll attempt to get the hang of it!

Well I sincerely liked studying it. This subject provided by you is very constructive for proper planning.